Credit Repair Service in Kansas

|

Kansas City Credit Repair Service is a team of credit repair experts here to provide the highest quality credit repair services in Kansas City. Our team of professionals has over 10 years of combined experience in assisting our customers to restoring their credit health, and ultimately leading to a more financially liberating, stress free lifestyle. Having poor credit in today's world can limit the options people have available to them in virtually every aspect of life, from renting a home or establishing an affordable mortgage, to purchasing a car or opening a new line of credit. The overall credit dispute process can feel overwhelming and time consuming for many people who simply do not have the time to banter back and forth with credit bureaus. That is why Kansas City Credit Repair Service is here to help eliminate the frustration and develop custom tailored plans that help guide our customers to total credit restoration.

|

Get StartedHassle Free, No Obligation

100% Privacy Guaranteed

|

Have poor credit? Give us a call.

Our Plans

Have Questions? Give us a Call.

816-399-2232

Credit Repair Kansas City

Credit Restoration in Kansas City

It is hard to navigate the current society with lousy credit. Quite a few companies use your credit history to decide whether to conduct business with you personally, and also to price goods and services that you use. Consumers with a distressed credit history frequently seek credit repair services to boost their credit in hopes of a more financially liberated life. As you browse credit repair services and weigh the smartest choices for your own credit health, here are the most vital things to understand about credit restoration.

You can certainly do it all yourself

Even though a respectable credit repair provider could be an alternative for some individuals, there is nothing that a credit repair company can do to you which you can not do on your own. There is lots of information out there in books and online that you may use to educate yourself about how credit works and everything you could do in order to fix your credit. Eliminating negative remarks can be carried out using effective methods including credit account disputes, debt investigation, pay for delete, and goodwill letters -- the typical plans credit repair businesses use to acquire negative information removed from your credit report. Doing this not only saves you money, but in addition, provides you control and power over your credit rating. As soon as you understand the credit repair strategies, you may use them anytime in the long run, should it becomes necessary.

Credit repair is all about your credit score, not your credit rating

Your credit rating is affected by the info in your credit . This is the reason why checking your credit history is the initial step to fixing your credit so you can determine the remarks that are damaging your credit rating and need to be disputed. Seeing your credit rating is beneficial as a fast means to tell if your credit is good, poor, or enhancing. A very low credit score suggests a bad credit history, which requires work. As your credit rating improves, it is a sign your credit history is significantly advancing. Purchasing your credit rating every time that you would like to determine where you stand could get pricey. Employing a free credit rating service such as Credit Karma or Credit Sesame will let you observe your own credit advancement at no price. If you are registering for a credit monitoring service, start looking for one that does not request a form of payment. Otherwise, there is a chance that you might be enrolling in a free trial subscription, which will start charging you every month if you don't cancel these subscriptions.

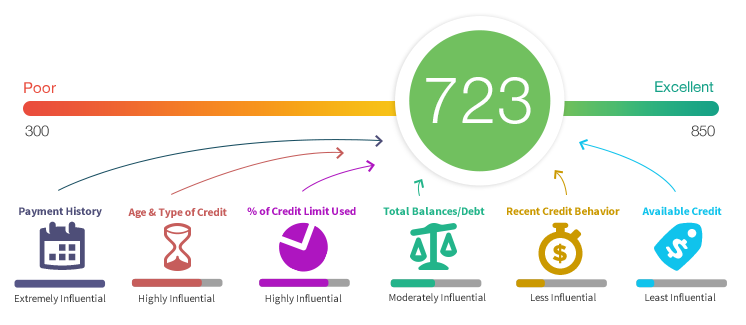

Your credit rating is based on five classes of data: payment history, amount of debt, the age of credit history, types of credit accounts, and recent applications for credit. Improving your credit in all these regions will enhance your credit rating overall.

Eliminating true negative advice is difficult.

Notice the accent on true. Credit reporting agencies are only legally bound to get rid of inaccurate or unverifiable information from the credit report. When correctly reported negative remarks hurt your credit score, it is tougher to eliminate this info because the credit reporting agencies are in their own rights to document this info. Actually, the integrity of the credit score system is dependent upon credit agencies reporting all precise information, even information that is negative. There are a few approaches to remove accurate negative information -- such as a set account to get a debt that you officially owe. These strategies can take additional time and effort compared to a simple credit score dispute. For these kinds of account debt validation (for collection agencies), pay for delete, and also goodwill deletion requests would be the best choices.

Doing nothing may be a plan

Negative information will not remain on your credit report indefinitely. Many negative remarks are only going to remain on your credit history for seven years. However, there are a couple exceptions. Chapter 7 bankruptcy and outstanding tax exemptions can remain on your credit score for as long as ten years. When an account is nearing the credit time limitation, waiting for it to drop off might be less stressful and time consuming than attempting to take out the accounts together with dispute letters or comparable plans. In contrast, taking actions on a drawback account doesn't prolong the credit reporting period limitation. Consequently, if you repay an outstanding debt, it will still fall off your credit report following year. Some newer versions of FICO and VantageScore don't contain paid collections on your credit rating. Closing accounts will not help. There is a common belief that only open balances are contained in an individual's credit report, and closing an account may eliminate it from their credit score. Unfortunately, in rare instances, shutting down an account may actually damage your credit rating. Closing an account will not eliminate it from the credit report. All of the details concerning the closed accounts will continue to be recorded on your credit history according to your creditors.

You are going to want open, live accounts using a positive payment history to enhance your credit rating. Opening new accounts using a poor credit rating can be challenging, so rehabilitating the account you have open may be easier.

Most credit repair businesses make lofty claims, such as promises they can not keep or bill upfront fees and don't deliver to their customers. Technically, these is prohibited by Federal law, but customers that are not knowledgeable about the law would not recognize that they were taken advantage of before it is too late. Over the previous several decades, the Federal Trade Commission has chased tons of credit repair firms who've violated the law. These organizations are often required to pay hefty penalties and sometimes are prohibited from doing business in the credit repair market due to their lack of reliability and scam like methods of operation.

A couple of tell tale signs that you are dealing with a dishonest credit firm could be:

Be on the lookout for credit restoration scams like these be ensuring that you understand the major red flags when dealing with a credit repair service.

You can not expect fast results. It requires some time to rebuild a poor credit history. Your credit rating follows your latest credit history significantly more than old remarks. A fantastic credit history generally includes a minimum number of adverse entries and a lot of recent favorable credit details. A couple of months of on-time obligations is really an ideal step in the right direction, but it will not offer you outstanding credit straight away. As time goes on and the adverse information drops off or gets old, and you replace it with favorable new info, you are going to start to notice your credit score slowly improving. Your credit rating may fluctuate through the credit repair procedure since the data in your credit report varies. Concentrate on the overall upward trajectory of your credit rating over a longer period of time.

Your improved credit will not survive if you do not change your habits.

A lot of men and women who seek credit repair -- if doing this themselves or hiring a business -- could get a simple loan, or get a mortgage or car loan. If you'd like your great credit to continue, you need to adopt habits that can maintain decent credit. This implies borrowing just what you can realistically afford to repay (and perhaps even a bit less). Paying your bills on time is among the greatest things that you can do to help your credit score. Lenders want to see that you have been in a position to fulfill your financial obligations on time every month. Thus, paying invoices on time is a significant, basic behavior to develop and maintain early.

You can certainly do it all yourself

Even though a respectable credit repair provider could be an alternative for some individuals, there is nothing that a credit repair company can do to you which you can not do on your own. There is lots of information out there in books and online that you may use to educate yourself about how credit works and everything you could do in order to fix your credit. Eliminating negative remarks can be carried out using effective methods including credit account disputes, debt investigation, pay for delete, and goodwill letters -- the typical plans credit repair businesses use to acquire negative information removed from your credit report. Doing this not only saves you money, but in addition, provides you control and power over your credit rating. As soon as you understand the credit repair strategies, you may use them anytime in the long run, should it becomes necessary.

Credit repair is all about your credit score, not your credit rating

Your credit rating is affected by the info in your credit . This is the reason why checking your credit history is the initial step to fixing your credit so you can determine the remarks that are damaging your credit rating and need to be disputed. Seeing your credit rating is beneficial as a fast means to tell if your credit is good, poor, or enhancing. A very low credit score suggests a bad credit history, which requires work. As your credit rating improves, it is a sign your credit history is significantly advancing. Purchasing your credit rating every time that you would like to determine where you stand could get pricey. Employing a free credit rating service such as Credit Karma or Credit Sesame will let you observe your own credit advancement at no price. If you are registering for a credit monitoring service, start looking for one that does not request a form of payment. Otherwise, there is a chance that you might be enrolling in a free trial subscription, which will start charging you every month if you don't cancel these subscriptions.

Your credit rating is based on five classes of data: payment history, amount of debt, the age of credit history, types of credit accounts, and recent applications for credit. Improving your credit in all these regions will enhance your credit rating overall.

Eliminating true negative advice is difficult.

Notice the accent on true. Credit reporting agencies are only legally bound to get rid of inaccurate or unverifiable information from the credit report. When correctly reported negative remarks hurt your credit score, it is tougher to eliminate this info because the credit reporting agencies are in their own rights to document this info. Actually, the integrity of the credit score system is dependent upon credit agencies reporting all precise information, even information that is negative. There are a few approaches to remove accurate negative information -- such as a set account to get a debt that you officially owe. These strategies can take additional time and effort compared to a simple credit score dispute. For these kinds of account debt validation (for collection agencies), pay for delete, and also goodwill deletion requests would be the best choices.

Doing nothing may be a plan

Negative information will not remain on your credit report indefinitely. Many negative remarks are only going to remain on your credit history for seven years. However, there are a couple exceptions. Chapter 7 bankruptcy and outstanding tax exemptions can remain on your credit score for as long as ten years. When an account is nearing the credit time limitation, waiting for it to drop off might be less stressful and time consuming than attempting to take out the accounts together with dispute letters or comparable plans. In contrast, taking actions on a drawback account doesn't prolong the credit reporting period limitation. Consequently, if you repay an outstanding debt, it will still fall off your credit report following year. Some newer versions of FICO and VantageScore don't contain paid collections on your credit rating. Closing accounts will not help. There is a common belief that only open balances are contained in an individual's credit report, and closing an account may eliminate it from their credit score. Unfortunately, in rare instances, shutting down an account may actually damage your credit rating. Closing an account will not eliminate it from the credit report. All of the details concerning the closed accounts will continue to be recorded on your credit history according to your creditors.

You are going to want open, live accounts using a positive payment history to enhance your credit rating. Opening new accounts using a poor credit rating can be challenging, so rehabilitating the account you have open may be easier.

Most credit repair businesses make lofty claims, such as promises they can not keep or bill upfront fees and don't deliver to their customers. Technically, these is prohibited by Federal law, but customers that are not knowledgeable about the law would not recognize that they were taken advantage of before it is too late. Over the previous several decades, the Federal Trade Commission has chased tons of credit repair firms who've violated the law. These organizations are often required to pay hefty penalties and sometimes are prohibited from doing business in the credit repair market due to their lack of reliability and scam like methods of operation.

A couple of tell tale signs that you are dealing with a dishonest credit firm could be:

- They request you pay upfront prior to any services start

- Cite a lawyer in connection with the authorities or distinctive connection with the credit reporting agencies

- Guarantee a particular credit rating

- Guarantee to delete precise information from the credit file

- Don't notify you of your right to dispute information directly with the credit reporting agencies

- Request that you waive your rights under the Credit Repair Organizations Act

Be on the lookout for credit restoration scams like these be ensuring that you understand the major red flags when dealing with a credit repair service.

You can not expect fast results. It requires some time to rebuild a poor credit history. Your credit rating follows your latest credit history significantly more than old remarks. A fantastic credit history generally includes a minimum number of adverse entries and a lot of recent favorable credit details. A couple of months of on-time obligations is really an ideal step in the right direction, but it will not offer you outstanding credit straight away. As time goes on and the adverse information drops off or gets old, and you replace it with favorable new info, you are going to start to notice your credit score slowly improving. Your credit rating may fluctuate through the credit repair procedure since the data in your credit report varies. Concentrate on the overall upward trajectory of your credit rating over a longer period of time.

Your improved credit will not survive if you do not change your habits.

A lot of men and women who seek credit repair -- if doing this themselves or hiring a business -- could get a simple loan, or get a mortgage or car loan. If you'd like your great credit to continue, you need to adopt habits that can maintain decent credit. This implies borrowing just what you can realistically afford to repay (and perhaps even a bit less). Paying your bills on time is among the greatest things that you can do to help your credit score. Lenders want to see that you have been in a position to fulfill your financial obligations on time every month. Thus, paying invoices on time is a significant, basic behavior to develop and maintain early.

Call today to start developing your credit repair plan